Published March 5, 2026

IPC and Seller Concession Limits (Explained)

The Mortgage Professional’s Cheat Sheet: IPC and Seller Concession Limits (Explained)

If you have ever heard “seller concessions” or “IPC” and thought, OK, but how much can we actually ask for, this is the plain-English breakdown of the infographic.

What is IPC?

IPC stands for Interested Party Contributions. In real estate terms, it is money contributed by someone with an interest in the transaction, usually the seller, to help pay some of the buyer’s closing costs and prepaid items.

Most people simply call this seller concessions or seller-paid closing costs.

Why do seller concession limits exist?

Lenders and investors (Fannie Mae, Freddie Mac, FHA, VA, USDA) cap concessions to reduce risk and prevent deals from being structured in a way that inflates price while quietly funding too much of the buyer’s costs.

In other words: concessions are allowed, but only up to certain limits based on loan type and sometimes down payment size.

The Big Picture Summary

The infographic breaks concessions into three main buckets:

- Government-backed loans (FHA, USDA, VA)

- Conventional primary and second homes (limits depend on down payment)

- Conventional investment properties (tighter limits)

Let’s walk through each.

1) Government-Backed Loans

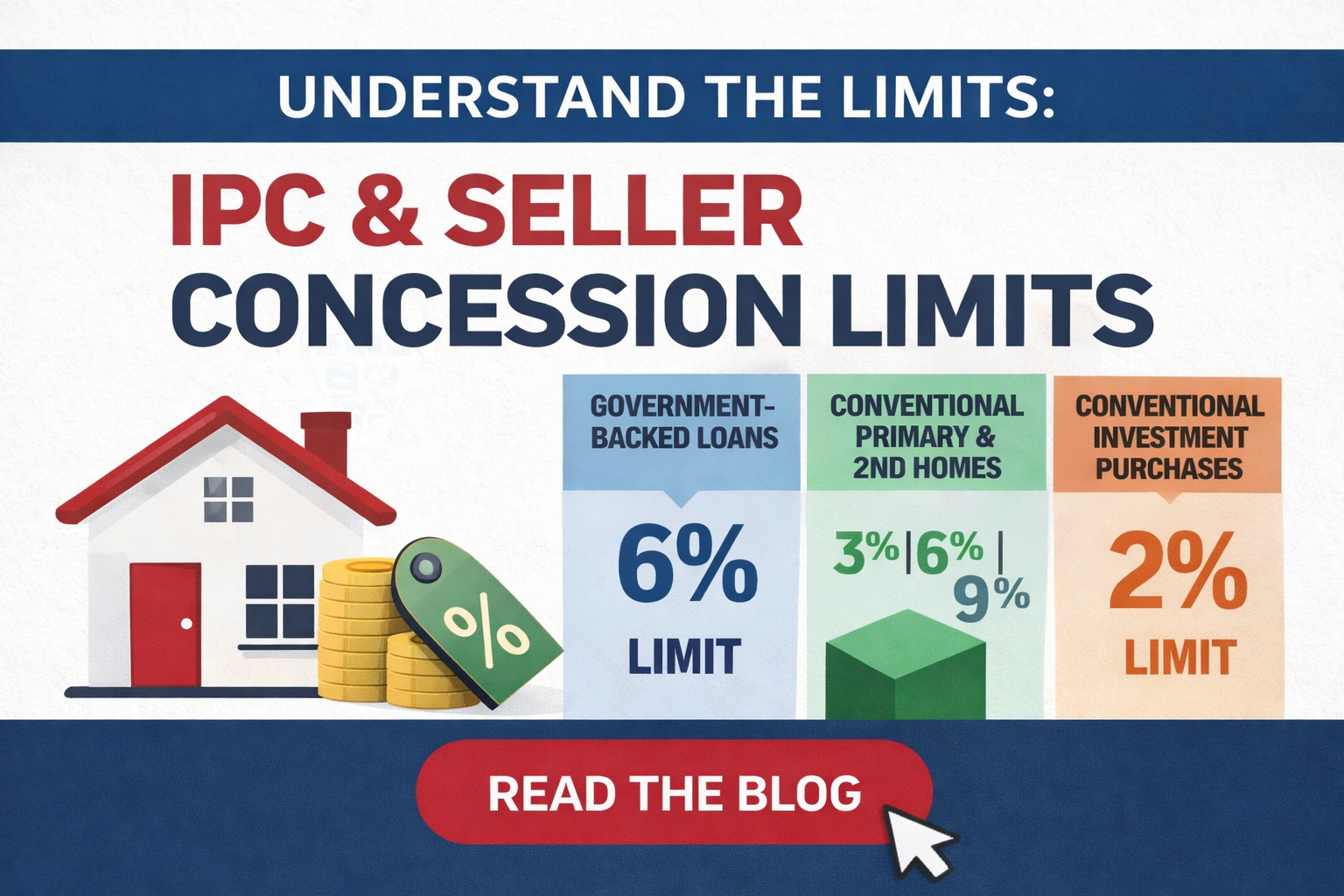

FHA and USDA: Up to 6% maximum

According to the infographic, FHA and USDA allow up to 6% of the sales price in interested party contributions toward the buyer’s costs.

Why this matters: FHA and USDA are common for first-time buyers and buyers with smaller down payments. Seller concessions can be a powerful tool to keep the buyer’s cash needed to close lower, especially when closing costs feel like a surprise.

Typical uses include:

- Loan closing costs (lender fees, title fees, escrow fees)

- Prepaids (insurance, taxes, prepaid interest)

- Approved items depending on the program and lender

VA: 4% limit with major caveats

The infographic highlights VA has a 4% limit, but with big caveats.

What this usually means in practice:

- The VA often allows certain costs to be paid by the seller in addition to the standard “4% concession cap,” depending on how costs are categorized.

- VA is known for having unique flexibility, including the ability for seller contributions to help with items that may not be allowed in the same way on other loan types.

Plain-English takeaway: VA can be flexible, but it is also detail-heavy. Your lender needs to structure it correctly.

2) Conventional Loans: Primary and Second Homes

For conventional financing (think Fannie Mae and Freddie Mac), the concession cap often depends on the down payment percentage.

Less than 10% down: 3% limit

If a buyer puts less than 10% down, the infographic shows a 3% concession limit.

Why: smaller down payments are higher risk, so concession flexibility is reduced.

10% to 25% down: 6% limit

If the down payment is 10% to 25%, the infographic shows a 6% limit.

This is a sweet spot where many buyers can still negotiate meaningful concessions, particularly in shifting markets.

More than 25% down: 9% limit

If the buyer puts more than 25% down, the infographic shows a 9% limit.

Translation: the more skin in the game the buyer has, the more flexibility lenders allow for seller contributions.

3) Conventional Investment Properties

This is where things tighten up.

Traditional conventional investment: 2% limit

The infographic shows a 2% limit for conventional investment purchases.

Why it matters: Investors often try to optimize leverage and cash-to-close. The rules restrict how much the seller can contribute under standard conventional investment guidelines.

Special programs exception: Up to 6%

The infographic also notes that some non-conventional investor programs (example: DSCR or bank statement style lending) may allow concessions up to 6%, depending on the lender and the specific program.

Important note: This is very lender-specific. The program rules, overlays, and what is permitted can vary a lot.

What counts as “seller concessions” in real life?

Seller concessions are most often used for:

- Buyer closing costs (title, escrow, lender fees)

- Prepaids (insurance, taxes, prepaid interest)

- Rate buydowns (temporary or permanent), if allowed by the program and lender structure

The infographic also hints at an important concept: some costs may be excluded from certain caps depending on loan type and how the costs are categorized.

This is exactly why the lender matters. Two deals can look identical on paper and get totally different answers depending on how the lender structures it.

Practical examples (how this plays out)

Example 1: FHA buyer wants help with closing costs

- Purchase price: $300,000

- FHA concession limit: 6%

- Max potential concessions: $18,000

In practice, the actual usable amount may be less depending on total closing costs and what the lender allows to be credited.

Example 2: Conventional buyer with 5% down

- Conventional primary residence

- Down payment < 10%

- Concession cap: 3%

If the market supports it, you might negotiate a concession, but you are playing within a smaller ceiling.

Example 3: Investor using conventional financing

- Investment property

- Cap: 2%

This is one reason many investors either bring more cash, negotiate price instead of concessions, or use alternative programs if they want higher concessions.

The bottom line

Seller concessions are one of the cleanest negotiation tools we have, but the allowable amount depends on:

- Loan type (FHA, USDA, VA, conventional)

- Occupancy (primary, second home, investment)

- Down payment size (for conventional primary and second homes)

- Program specifics and lender overlays

If you are thinking of using concessions in an offer or a counteroffer, the best move is to align three people early:

- buyer

- agent

- lender

Because the deal only works if the structure works.

Quick disclaimer

This post is educational and based on the infographic overview. Loan guidelines can change, and lenders can apply overlays. Always confirm concession limits and eligible costs with the buyer’s lender for the specific transaction.